Fund your overseas degree the smart way

The financial side of studying abroad is where most Indian families lose lakhs — bad loan terms, wrong sponsor structure, missed 80E deductions, poor forex timing. We've structured funding for 5,000+ students since 2008 across HDFC Credila, ICICI, Axis, Avanse, InCred, Prodigy, and MPower — and we know which one fits which profile.

take commission from lenders

What end-to-end financial planning from ESM covers

Not a single loan referral. A full funding strategy — from loan structuring to scholarship search to forex planning to repayment optimisation.

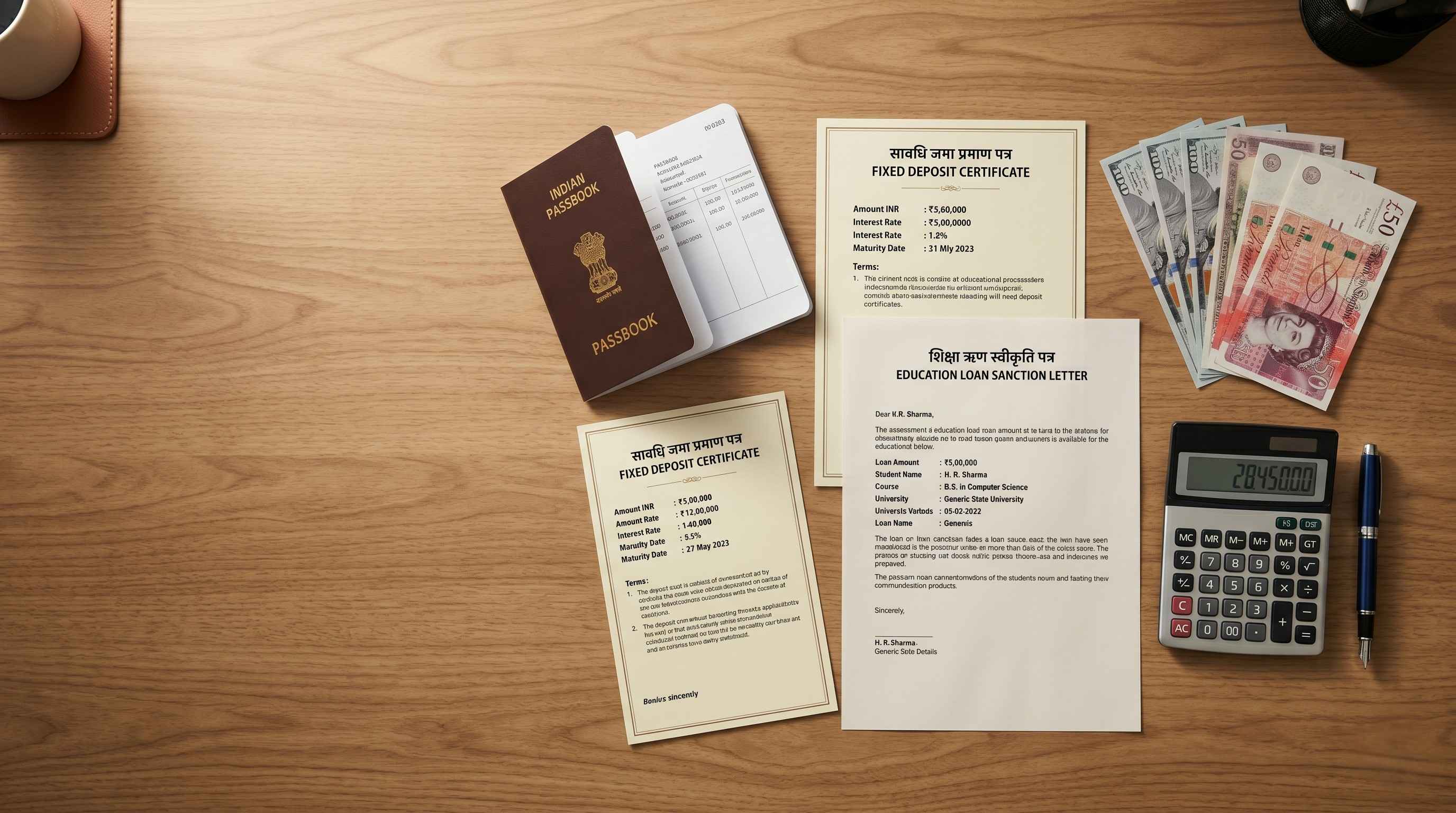

Education loan structuring

Collateral vs. non-collateral, Indian bank vs. NBFC vs. overseas lender (Prodigy, MPower), co-applicant strategy, moratorium length — we match the structure to your profile.

Scholarship search & applications

University-specific awards, country government schemes (Chevening, Fulbright, Vanier), Indian gov schemes (NOS, Inlaks, KC Mahindra). We help identify and apply to the ones you actually qualify for.

Sponsor letters & FD structuring

For visa proof, the way your financial story is structured matters more than the total amount. We organise FDs, savings, and sponsor letters in the exact pattern each consulate expects.

GIC account setup (Canada)

The CAD 20,635 Guaranteed Investment Certificate is mandatory for the Canada SDS route. We coordinate with Scotiabank, ICICI Canada, CIBC, or HSBC depending on your situation.

Forex management

Wire transfer vs. forex card vs. demand draft — each has different fees and exchange rate spreads. We recommend strategies that save typical families ₹50,000–₹2 lakh per year abroad.

Tax & repayment planning

Section 80E lets you deduct the full interest on your education loan from taxable income — without any cap. We also plan TCS implications and your post-graduation EMI structure.

Financial planning insights

Loan deep-dives, scholarship updates, tax tips, and real funding stories from our Chandigarh team.

Funding advice from people with no commission to chase

Most loan agents you’ll meet are paid a percentage by the lender — which biases them toward whichever lender pays them the most, not the one that fits you best. ESM’s financial planning is part of our service fee, not a commission-driven sale.

Result: when we tell you HDFC Credila has better rates than ICICI for your profile, or that Prodigy makes more sense than an Indian NBFC for a US Master’s, or that GIC + part-loan beats full loan for Canada — you can trust we’re saying it because it’s true, not because it pays our office better.

18 years of loan + scholarship work

Thousands of student funding cases handled since 2008 across all 7 countries — that institutional memory shapes every recommendation.

Direct lender relationships

Active working relationships with HDFC Credila, ICICI, Axis, Avanse, InCred, Auxilo, Prodigy Finance, and MPower Financing. We know each lender’s actual decision criteria.

Country-specific financial knowledge

GIC for Canada, MOE Tuition Grant for Singapore, NHS surcharge for UK, SEVIS fee for US — each country has unique cost components most agents miss.

Tax-optimised structures

80E deduction routing, TCS rate-class selection (20% vs 0.5%), LRS limit management. We design the funding flow to legally minimise tax leakage on remittances.

Zero commission, zero bias

We earn nothing from lenders. So when we recommend a lender, you know it’s because they’re the right fit — not because they pay the highest agent commission.

Walk-in office in Chandigarh

SCO 375-376, Sector 35B. Walk in Mon–Sat 9:30 AM–6:00 PM, or book a video call if you’re outside Chandigarh.

How an ESM financial planning engagement actually unfolds

Four phases, each with clear deliverables. You always know what stage you're at and what comes next.

Financial profile assessment (FREE)

Your family income, existing assets, collateral availability, academic profile, and target country. We give you a frank read on what funding mix is realistic — loan, scholarship, sponsor, or a combination — with no payment until you decide to proceed.

Funding strategy design

We map a complete funding plan: which lenders to approach, what loan amount to target, which scholarships to apply for, how to structure sponsor letters, and how to optimise tax through 80E. You get a written funding roadmap.

Loan structuring & applications

We coordinate the loan applications across 2–3 lenders simultaneously, prep the documentation each one wants, structure your co-applicant case, and negotiate terms where possible. Approval usually comes in 7–15 days.

Disbursement & ongoing forex support

We coordinate disbursement timing with university fee deadlines, advise on wire transfer vs. forex card timing, and help with GIC setup or sponsor remittance. Support continues as your financial needs evolve abroad.

Financial planning makes sense if you’re...

Most families fall into one of these four situations. If yours doesn't fit cleanly, that's fine too — the first review is free, come talk.

A student needing an education loan

Whether you have collateral (property, FD) or not, whether co-applicant has strong credit or not — loan structuring varies hugely. We map your profile to the right lender mix and negotiate terms.

A family demonstrating funds for visa proof

You’re self-funding or partially self-funding — but how those funds are structured in your bank statements, FDs, and sponsor letters dramatically affects visa approval. We structure the financial story for the consulate.

A scholarship-eligible student

Strong academics, financial-need-based, or merit-based — you may qualify for university scholarships, country gov schemes (Chevening, Fulbright), or Indian schemes (NOS, Inlaks, Tata Trusts). We identify and help you apply.

A Canada or UK SDS aspirant

Canada SDS needs GIC + first-year tuition deposit. UK Standard requires 28 days of held funds. These streamlined visa categories have specific funding patterns — we set them up correctly the first time.

Hear from ESM students directly

Short video stories from real students we’ve counselled and placed. Tap any thumbnail to watch on YouTube.

Financial planning questions answered

Ready to get your funding plan sorted?

Talk to an ESM counsellor who has placed thousands of Indian families who funded overseas degrees the smart way — through structured planning, not last-minute decisions. We'll review your profile and map out your next steps — free, no obligation.